热点栏目

热点栏目来源:市川新田三丁目

译者 王为

ByKathy Jones

As expected, Federal Reserve Chair Jerome Powell announced a shift in policy that stems from a year-long review that the Fed has done. In a speech entitled “Navigating the Decade Ahead,” the key shift in policy is a move to an “average inflation” target instead of a precise 2% target. The change suggests that the Fed will likely maintain its zero-interest-rate policy for several more years until it sees inflation rise, rather than acting pre-emptively to address inflation expectations.

不出所料,在经过长达一年的审视后,美联储主席鲍威尔宣布对货币政策目标作出重大调整。在昨晚发布的题为“探领未来十年”的演讲中,鲍威尔勾勒的货币政策变动是将通胀增速目标从2%的明确数值调整为“在一段时间内通胀率均值达标”。这一转变意味着联储有可能在未来数年内继续维持当前的零利率政策,而不会在应对通胀预期上升方面“打提前量”。

Bygones are no longer bygones

该翻过去的一页

The Fed’s shift in policy implies that it will allow inflation to run at a pace above 2% for a period of time to offset the undershooting of inflation over the past decade. It is often referred to as letting inflation run “hot” for a while—although it’s hard to argue that 2.5% to 3.0% inflation is “hot.” In the past, the Fed viewed each inflation reading discretely. The past was gone, and all that mattered was the present and prospects for inflation based largely on the unemployment rate.

货币政策方面的重大调整意味着联储将容忍美国通胀增速在一段时期里超过2%以抵消过去十年通胀增速不达标所造成的影响,这一做法经常被解读为允许通胀率在一定期间内“有点过热”,尽管很难说2.5%至3.0%的通胀增速是否就是“有点过热”。以往美联储总是对通胀指标具体情况具体分析,但那都是以往的做法了,现在最要紧的是眼前的局势以及未来在很大程度上基于就业率表现的通胀预期。

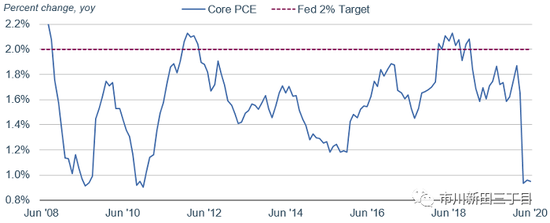

Inflation has fallen short of 2% for most of the past decade

在过去十年中的大多数年份里美国通胀增速没有达到2%的通胀目标

Source: Bloomberg. Personal Consumption Expenditures: All Items Less Food & Energy (Core PCE) (PCE CYOY Index), percent change, year over year. Monthly data as of 6/30/2020.

图表信息来源:彭博资讯,指标为美国个人消费开支指数核心值的年度同比百分比变化,不含食品和能源价格涨幅,数值截止日期为2020年6月30日

The reasoning behind the Fed’s change in policy is the evidence that the relationship between the unemployment rate and inflation has changed. Lower levels of unemployment have not led to higher inflation during the past 10 to 15 years, as they had in previous years. In addition, the Fed has determined that demographic changes, such as the aging of the population along with slowing productivity growth, have led to a decline in the economy’s potential growth rate. The Fed’s estimate of potential gross domestic product growth has dropped to 1.8% from 2.5% in 2012. In turn, that suggests that the level of short-term interest rates associated with stable inflation is lower than in the past. The “neutral” federal funds rate is estimated at 2.5%, compared with 4.2% in 2012.

联储对货币政策作出调整的原因在于美国失业率和通胀率之间的关联关系发生了变化。在过去10-15年里,低失业率并没有像以往那些年份一样带来高通胀。此外,联储还认为美国人口结构方面的变化,比如在生产率放缓的同时人口老龄化问题开始日渐严重,导致潜在经济增速出现下降。联储测算结果显示,美国国内生产总值的潜在增速已从2012年的2.5%跌至当前的1.8%。反过头来意味着,与稳定的通胀增速相关联的美国短期利率的水平要低于以往。据测算,当前联邦基金利率的“中性水平”为2.5%,而2012年时为4.2%。

In announcing the Fed’s change in policy, Powell indicated that the fed funds rate would stay near zero until inflation rises above 2% “for some time.” The Fed has allowed itself a lot of flexibility, however. There is a heavy emphasis on achieving full employment, which now appears to be the Fed’s primary goal, considering that inflation remains quite low and unemployment very high.

在宣布联储货币政策变化的讲话中,鲍威尔指出除非美国通胀增速在一段时间里能跑到2%以上,否则联邦基金利率的水平应一直停留在0%附近。但是,联储也给自己留了不少余地。联储着重强调的是充分就业,这似乎已经成了联储当前最优先实现的政策目标,要知道当前美国的通胀率仍处于相当低的水平而失业率却很高。

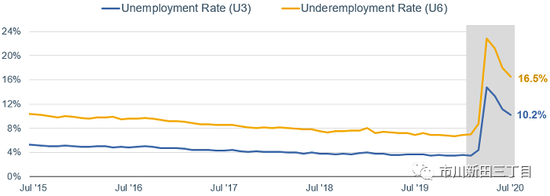

High unemployment is one of the Fed’s biggest concerns

联储心头最挂念的是高失业率

Source: Bureau of Labor Statistics.Civilian Unemployment Rateand Underemployment Rate, Total unemployed, plus all marginallyattachedworkers plus total employed part time for economic reasons (U6 Rate), Percent,Monthly, Seasonally Adjusted. Shaded area indicates recession. Monthly data asof July 2020.

图表信息来源:美国就业统计署,指标为美国个人失业率和非充分就业的比率,数值为经季节性调整的月度百分比,阴影部分为经济衰退时期,取值截止日期为2020年7月

What’s missing

本次讲话中没有提到的东西

Powell provided no indication ofhowthe Fed hopes to achieve higher inflation. That’s probably because the Fed has already expanded monetary policy dramatically, without lifting inflation. It can continue to keep short-term interest rates near zero, expand its balance sheet by buying more bonds to hold down long-term interest rates, and use its special facilities to lend. However, these tools are stretched already. Many Fed officials have been urging Congress to pass more fiscal relief, as that would likely have a more immediate effect in boosting growth, employment, and inflation.

鲍威尔没有提及联储希望采取何种手段以实现通胀率上升,这可能是因为联储已经对货币政策进行了大幅扩张但通胀率却并没有随之上升。联储可将短期利率的水平继续压制在0%附近,通过买入更多债券的方式扩张资产负债规模以拉低长期限利率的水平或者利用特别设立的流动性融资便利提供借款。但是,这些举措已经使用过度了。很多联储官员呼吁美国国会出台更多的财政纾困法案,因这样做有可能会在刺激经济成长、增加就业以及推升通胀增速方面见效更快。

Evolution, not revolution

联储政策转变是渐进的,而非革命性的

Powell’s speech is important in that it codifies the Fed’s approach to policy. However, it isn’t a big change from the way the Fed has been operating for a while now. It will help set expectations about policy by identifying the key factors that are important to the Fed. However, monetary policy can only do so much. The biggest risk to the policy shift is that long-term rates could rise on the assumption that the Fed would not respond to inflation fast enough to contain it.

鲍威尔讲话的重要意义在于将联储的思路通过一项具体的政策表述了出来。但从联储已经操作过一段时间的做法来看,这一政策性变化并不突兀,其讲话可以帮助大家了解哪些因素对联储来说至关重要,有助于市场对联储的货币政策进行预期,但货币政策能做的也不过如此。本次政策调整所面临的最大风险在于,美国长期限利率有可能出现上升,原因是市场假设联储在美国通胀增速上扬之时可能不会及时做出反应。

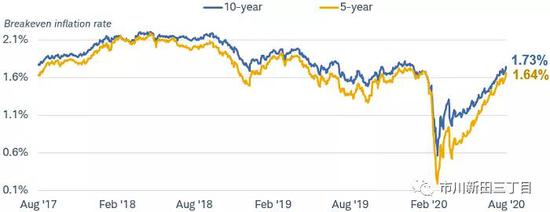

Inflation expectations have already been rising, but remain below 2%.The Fed could find itself needing to react more quickly than it would like to quell those expectations. Yield curve control could be employed at that stage—with the Fed buying longer-term bonds to hold down yields. That doesn’t appear to be a near-term issue, but it could be a longer-term issue.

市场对美国通胀增速的预期已出现了上升,但仍低于2%,也许联储会发现自己需要更加讯速地做出回应以平息通胀预期上升的势头。到了那一步联储可能会采取控制国债收益率曲线的手段,也就是买入长期限的美国国债以拉低国债收益率的水平。从短期来看这似乎并不是一个大问题,但长期来看不容忽视。

Market expectations for inflation have been rising but remain below 2%

市场对美国通胀增速的预期已出现了上升,但仍低于2%

Source: Bloomberg. U.S. Breakeven 10 Year (USGGBE10 Index) andU.S. Breakeven 5 Year (USGGBE05 Index). Daily data as of 8/27/2020.

图表来源:彭博资讯,指标为美国10年期和5年期通胀保值国债的临界通胀率,数值截止日期为2020年8月27日

Bottom line: The Fed’s policy announcement has reinforced our view. We look for the Fed to keep short-term interest rates low for several more years, and the U.S. dollar to weaken further over time.

要点:美联储宣布的政策变化进一步强化了我们原先的观点,我们认为联储在未来数年里会继续将短期利率的水平维持在低位,美元汇率会在未来一段时间里继续贬值。

版权及免责声明:凡本网所属版权作品,转载时须获得授权并注明来源“融道中国”,违者本网将保留追究其相关法律责任的权力。凡转载文章,不代表本网观点和立场。

延伸阅读

马斯克V.S薛其坤:立足当下 对人类未来展开无限想象

马斯克V.S薛其坤:立足当下 对人类未来展开无限想象

众安在线扭亏为盈:2020年净利5.5亿 数字生活生态驱动增长

众安在线扭亏为盈:2020年净利5.5亿 数字生活生态驱动增长

版权所有:融道中国